Costco Wholesale (COST) is a large membership warehouse retailer that sells a variety of bulk goods in several countries.

-Seven Year Revenue Growth Rate: 9.4% ![]()

-Seven Year EPS Growth Rate: 8.6%

-Seven Year Dividend Growth Rate: 13.3%

-Current Dividend Yield: 1.08%

-Balance Sheet Strength: Strong

Costco is one of the lowest yielding stocks that I publish analysis articles on when not taking into account their recent huge one-time special dividend.

Overall, much like last year, I think Costco is a fantastic company and a respectable stock for long-term capital appreciation, but at the current time, I view it as fully valued with little or no margin of safety, and it doesn’t offer a very appealing regular dividend yield.

Overview

Founded in 1983, Costco Wholesale (NASDAQ: COST) is a large warehouse-based retailer, primarily located throughout North America but with a presence in Europe and Asia as well.

With over 170,000 employees, Costco operates 622 warehouses. Of these, 448 are in the US and Puerto Rico, 85 are in Canada, 32 are in Mexico, 23 are in the UK, 13 are in Japan, 9 are in Taiwan, 9 are in Korea, and 3 are in Australia. In addition, Costco operates its large online retail site.

Category Sales

Costco warehouses offer various items, clothes, food, electronics, glasses, pharmacy drugs, gasoline, car-washes, and more. There are bulk items for cheap shopping, but there are select higher-end items.

Sundries (cleaning supplies, tobacco, alcohol, candy, snacks, etc.) accounted for 22% of 2011 sales.

Hardlines (electronics, hardware, office supplies, beauty supplies, furniture, garden, etc.) accounted for 16% of sales.

Food accounted for 21% of sales.

Softlines (clothing, housewares, small appliances, jewelry, etc.) accounted for 10% of sales.

Fresh food accounted for 13% of sales.

Ancillary and other (gas, pharmacy, food court, optical, etc.) accounted for 18% of sales. (This is their fastest growing segment, as they put more of these areas in newer Costcos.)

Ratios

Price to Earnings: 25

Price to Free Cash Flow: 24

Price to Book: 3.5

Return on Equity: 15%

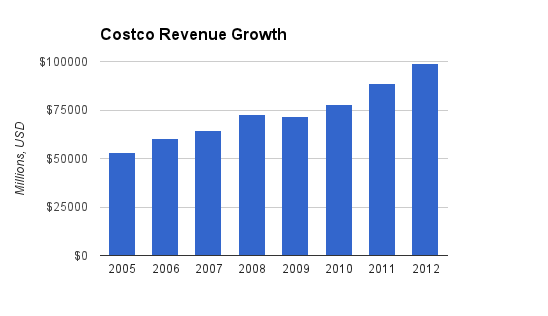

Revenue

(Chart Source: DividendMonk.com)

Revenue growth over this period has been particularly strong at 9.4% per year, which is quite substantial for a large and consistent company. Every year except 2009 had strong revenue growth

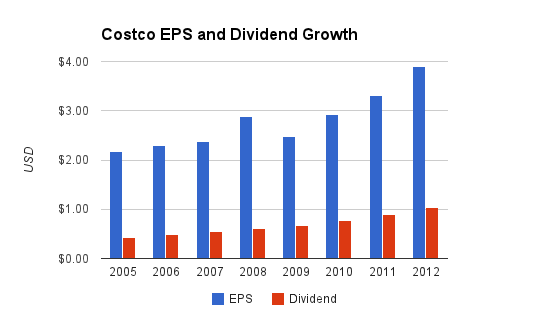

Earnings and Dividends

(Chart Source: DividendMonk.com)

EPS has grown by an average of 8.6% per year over this period. The growth has been fairly smooth with the exception of 2009.

Costco has a low dividend yield of only 1.08% as of this writing, and a dividend growth rate averaging 13.3% per year over the last seven years. I rarely cover companies with a yield that low, but Costco is an exception because the company quantitatively has all the characteristics of a dividend growth stock despite the fact that it will fall significantly below many income investors’ yield minimums. The payout ratio is on the low side at only around 25%, but as a comparison, that’s higher than Exxon Mobil and Aflac, and only a bit below Chevron, which are all classic dividend growth stocks that I publish reports on.

The low yield is the result of a combination of this fairly modest dividend yield and a fairly high valuation (PE of 25) rather than due purely to an extremely low payout ratio.

How Does Costco Spend Its Cash?

For the fiscal years 2010, 2011, and 2012, Costco brought in a total of approximately $5.2 billion in free cash flow. Over the same period, the company spent under $1.2 billion on dividends, $1.8 on net share buybacks, and under $1 billion on acquisitions. The company has reduced its share count by a bit over 10% over the last seven years, which isn’t a very large amount due the consistently robust valuation of the stock.

Unfortunately, in my Dividends vs. Share Repurchases article which I often reference, I use Costco as a prime example of a well-run company that makes suboptimal share repurchase decisions. Few would argue that Costco has not been exceptionally well-managed since its founding overall, and yet it is quantitatively demonstrable that the company is not making the best possible use of its cash when it comes to these buybacks. Costco is not alone in this; it’s the corporate norm.

For example, the Costco stock price has been on a smooth upward trajectory over the last 10 years, with the one big exception being during the financial crisis between late 2008 and throughout 2009 and into early 2010. The year of 2009 was a particularly low year for the stock. And yet, when one looks through their history of share repurchases, it turns out management spent a considerable amount of money on share repurchases every year since 2005, with the exception of 2009. When the stock price was at its lowest, Costco was hording cash and not buying, but when times are better, cash is flowing, and the stock valuation is higher, Costco liberally buys back more shares.

This is a consistent theme with American blue chip stocks. A Credit Suisse research study showed that broadly speaking across the market, share buyback amounts are positively correlated with stock price. In other words, the higher the stock value, the more companies are buying their shares back.

While Costco management has done a tremendous job in terms of total shareholder returns, wise shareholders would likely be slightly better off if the payout ratio was increased to a more moderate figure; perhaps in the 40-55% payout ratio range, at the cost of reduced share buybacks. Shareholders can decide to reinvest that money or not.

The recent $7 special dividend was in my opinion a good use of cash for shareholders. This won’t be a common thing, since it was based on the political environment and was worth a couple years worth of free cash flow generation by the company.

Balance Sheet

Before the special dividend, Costco had a very strong balance sheet with a total debt/equity ratio of under 11%. The total amount of debt was lower than the annual income and the interest coverage ratio was well over 30. Due to Costco’s low acquisition activity, goodwill hasn’t accumulated on the balance sheet.

The company tapped into this battery of capital to pay a huge $7 special dividend at the end of 2012 that is not yet reflected in a quarterly report. That was before there was a ‘Fiscal Cliff’ deal and changes in dividend tax rates were uncertain. It was prudent to pay a larger dividend while tax rates were known to be low. The company offered over $3 billion in debt to fund this dividend which cost over $3 billion to pay all shareholders. Based on the addition of debt and the subtraction from shareholder equity, Costco’s balance sheet will be a bit more leveraged but still fairly conservative.

A dividend of this magnitude shows specifically why a strong or weak balance sheet should be taken into account when valuing a stock. A strong balance sheet can act as a battery for shareholder returns should the opportunity arise, either in the form of dividends, buybacks, acquisitions, or core growth. When analyzing a stock with the Dividend Discount Model or Discounted Cash Flow Analysis, I generally take the strength of the balance sheet into account by allowing for a smaller margin of safety or by allowing for a slightly reduced discount rate.

Investment Thesis

Costco’s business model is meant to maximize efficiency. The warehouse format keeps costs low, as they buy and sell items in bulk. Shoppers (both consumers and small business owners) pay membership fees, and in return receive exceptionally low prices. The warehouse model also generally operates moderately reduced hours compared to typical retailers. Although Costco offers a large range of products, they limit their selections in each category to only the best-selling ones, so the number of individual products is actually lower than many other retailers (as in, less than 10% as many items as in a Walmart store) and they can maximize their purchasing power for these items. This further streamlines their business.

Costco’s memberships keep customers loyal, and they have a high renewal rate. Costco can keep its prices reasonably competitive with Wal-Mart by maintaining such a low profit margin. The company gets most of its profit from membership fees while its goods are sold at very low markups or even at losses.

Growth

| Year | Warehouses | Gold Star Members | Business Members |

|---|---|---|---|

| 2012 | 622 | 26.736 million | 6.442 million |

| 2011 | 592 | 25.028 million | 6.352 million |

| 2010 | 540 | 22.539 million | 5.789 million |

| 2009 | 527 | 21.445 million | 5.719 million |

| 2008 | 512 | 20.181 million | 5.594 million |

| 2007 | 488 | 18.619 million | 5.401 million |

Each year in this snapshot, as well as in many previous years, Costco increased their number of warehouses, and saw an increase in both gold star members and business members. As of the most recent report, Coscto has 622 warehouses as of the end of their fiscal year 2012.

Despite Costco’s mild setback in 2009 due to the recession, Costco became the 3rd largest retailer in the US compared to its spot at 5th in 2008, and is one of the largest retailers in the world as well.

Two Points for Bullishness

There are a couple key things I want to highlight that, in my view, make Costco not (quite) as overvalued as it seems.

1. Revenue growth is outstanding. Most large businesses aren’t growing revenue at nearly the pace of Costco. Costco’s number of stores is growing, their number of members is growing, and they have repeatedly demonstrated the ability to raise their membership prices without substantial drop-off rates.

2. Low profit margins can mean eventual upside. Costco is currently sacrificing profitability for solid ethics and market share growth. Costco is a viable competitor to even Walmart, and yet has only existed since the 1980’s. The larger the revenue becomes, the more pricing power they have, and the denser their store locations get, the more efficient they become. The net margin is currently under 2% compared to Walmart that has a profit margin of over 3%. The retail industry competes on price and has low profit margins across the board, so an increase of 25-50 basis points has a huge impact on the bottom line. Costco’s business of model of high employee pay and selling a larger amount of fewer products has resulted in extremely strong sales per square foot of retail space.

Risks

As a retailer, Costco is a middle-man, with limited pricing power, and the retail industry is incredibly competitive. Costco faces competition from warehouses like BJ’s and Sam’s Club (owned by Wal-Mart), general retailers like Wal-Mart, Target, and Kohls, as well as from online competitors like Amazon.

In addition, since the stock has a fairly high valuation, there is considerable risk of poor stock performance if Costco doesn’t continue to outperform as a company.

Conclusion and Valuation

Based on DCF analysis with a 10% discount rate, the current market cap of around $44 billion is justified if the company can grow free cash flow by 8% per year over the next 10 years followed by 4% per year perpetually thereafter, which is a rather aggressive estimate.

Alternatively, if those estimates are toned down to 7% growth for 10 years followed by 3% perpetual growth with a discount rate reduced to 9%, the current market cap is fair.

These estimates demonstrate that while the current valuation may not represent an overvalued stock, it likely doesn’t offer any significant margin of safety either.

With such a low yield, the stock is obviously not an ideal selection for investors that desire current income as part of their financial freedom. For investors that appreciate the qualities of Costco that make it a similar quantitative and qualitative investment to other dividend growth stocks but with a reduced yield, it may be a decent selection for long term capital appreciation.

I believe Costco stock will continue to increase in price over the long-term, but at the current time with the stock a bit over $102/share, I observe that there are likely better (and significantly higher yielding) dividend growth investments out there.

Full Disclosure: As of this writing, I have no position in COST.

You can see my dividend portfolio here.

Strategic Dividend Newsletter:

Sign up for the free dividend and income investing newsletter to get market updates, attractively priced stock ideas, resources, investing tips, and exclusive investing strategies:

I recently watched a documentary about Costco on CNBC, which got me interested in the company. It is essentially making all its profits from membership fees (as your analysis showed also) I researched the company and it looked like it has a lot of growth ahead of it. My issue is that it is trading above 20 times earnings. EPS are projected at $4.50 in 2013 and $5 in 2014 vs $3.89 for 2012. If it fell below $80/share, I might get a small position despite the fact that current yield is low.

As usual, a very nice analysis. I like Costco as a company and would love to buy them. But with a starting yield floating around 1%, the company is a poor choice for my dividend growth based strategy that is geared towards achieving early financial independence.

Wasn’t it a good move from Costco to be hoarding cash when nobody knew what would happen? For me it is a good sign of being responsible.

Great article! Jim Cramer has been touting this stock for quite some time now. Costco is a much better run company than Walmart and Target. The company still hasn’t saturated the market either.

Costco is unbeatable and will make money for you in future if you buy and hold.