AFLAC Incorporated (AFL) is a supplemental insurer with a large presence in Japan, as well as the 50 US states.

![]()

-Revenue Growth Rate: 7.6%

-EPS Growth Rate: 7.5%

-Book Value Growth Rate: 9.9%

-Dividend Growth Rate: 18.3%

-Current Dividend Yield: 2.88%

-Balance Sheet: European Debt Exposure

Aflac’s core performance has been remarkable over the last decade. The company, however, does have more than $5.6 billion in debt exposure to a combination of Portugal, Italy, Ireland, and Spain.

Overview

AFLAC Incorporated (NYSE: AFL) is a large international supplemental insurer. They provide cash that can cover several types of expenses to those receiving payouts due to illness or deaths. This is supplementary to primary medical insurance which helps cover medical expenses but leaves other expenses without a solution. This Fortune 500 company was founded in 1955, and has a large presence in Japan and the US. AFLAC stands for the American Family Life Assurance Company.

The company made a big move in Japan in the 1970s by selling insurance for cancers when people were becoming particularly mindful of cancer. Decades later, approximately three-quarters of Aflac’s diverse premiums now come from Japan.

Aflac primarily targets places of employment for its insurance products, rather than individuals outside of work. The company offers plans to employers that allow them to provide Aflac insurance as part of their benefits package without paying any cost themselves.

The premise behind an insurance company is that they spread risk out over a wide number of people and businesses. They collect premiums (payments) from clients and in return those clients are covered in case of a serious loss. From an insurance business standpoint, it’s ideal to collect more in premiums than you pay out for losses. This is not the primary form of earnings, though. An insurance business, after collecting all of the premiums, holds a great deal of assets that, over time, are paid out for client losses. An insurance company constantly receives premiums and pays out for losses, so as long as they are prudent with their business, they get to constantly keep this large sum of stored-up assets. As any investor reading this knows, a great sum of money can be used to generate income from investments, and that’s how an insurance company really makes money. Aflac invests its stored up collection of assets primarily in fixed income securities to receive upwards of $3 billion in annual investment income.

Ratios

Price to Earnings: 9

Price to Book: 1.5

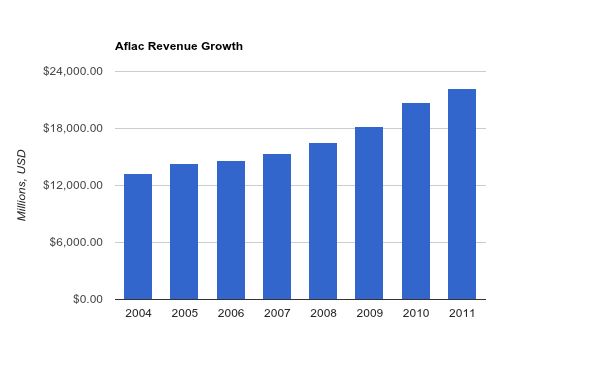

Revenue

(Chart Source: DividendMonk.com)

Aflac has had particularly strong core business performance over the last decade. Revenues from both premium income and investment income have increased every year for at least the last ten consecutive years. The annualized revenue growth rate over the last seven years was 7.6%.

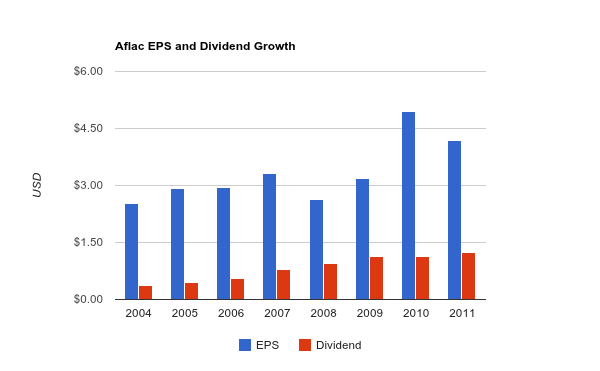

Earnings and Dividends

(Chart Source: DividendMonk.com)

Aflac has had somewhat erratic EPS numbers, but the average growth over this seven year period was 7.5% per year. EPS spiked to $5.49 over current the trailing twelve month period, which the chart doesn’t show. The company’s operating earnings per share, which excludes yen currency effects, impairments, and certain other items, has increased every year for over two consecutive decades.

As for the dividends, Aflac has increased the dividend every year since the early 1980’s. The payout ratio is rather low, at under 25%. This has allowed for the dividend to grow more quickly than EPS. Despite the low payout ratio, the dividend yield is pretty substantial at 2.88%, because the stock valuation is so low.

Approximate Historical Dividend Yield at Beginning of Each Year:

| Year | Yield |

|---|---|

| Current | 2.88% |

| 2012 | 3.00% |

| 2011 | 2.10% |

| 2010 | 2.30% |

| 2009 | 2.10% |

| 2008 | 1.30% |

| 2007 | 1.40% |

| 2006 | 0.90% |

| 2005 | 1.00% |

| 2004 | 0.90% |

The current yield of 2.88% is higher than it has been historically, with exceptions for dips in early 2009 and late 2011.

Balance Sheet

Aflac has substantial exposure to European debt. More specifically, out of their $104.6 billion portfolio, more than $5.6 billion of those debt holdings are from a combination of Portugal, Italy, Ireland, and Spain, with Italy and Spain making up the bulk of that segment. And this figure comes after the company has taken moves to reduce risky European debt exposure and after they’ve already realized billions in losses. The company has broad and safe debt exposure mainly to Japan, and also to the U.S. and financially stronger portions of Europe, but this “PIIGS” exposure remains a risk.

Investment Thesis

Aflac has a notable business model. Rather than targeting individuals, Aflac insurance agents target businesses. Aflac works with employers to give employees the option to purchase Aflac Insurance via payroll deductions, similar to their other benefits. This “cluster-selling” technique keeps costs comparatively low, and gives the company a major competitive price advantage. It creates a win-win situation with employers it does business with.

In addition to having a solid distribution network for its insurance products, Aflac has a strong brand name that is well known in Japan and US, with the duck mascot. The brand is stronger than most other insurers, especially in Japan.

Plus, its insurance is rather resistant to health care reform or other insurance regulation (although not untouched). The company provides supplemental insurance; cash to people when they need it most.

The company has been recognized as one of the “World’s Most Ethical Companies” by Ethisphere Magazine, and also one of the best places to work. It has won similar awards from a variety of sources.

Aflac’s US exposure is significantly smaller than its Japanese exposure despite being a US-based company. Their customer retention rates are not as high in the US as they are in Japan, but the other side to this is that there is more growth and improvement opportunity.

The Problem

So why the low valuation? The company is trading at under 9 times current earnings, and under 7 times forward earnings. The reason is the portolio’s exposure to European sovereign and financial debt. Aflac is currently restructuring its portfolio to reduce risk, and this is resulting in realized losses. For example, the company closed out a large position in Greek financial institution debt, and reduced positions in certain other European banks. The market is clearly factoring in continued restructuring.

Having between 5% and 6% of the total portfolio in these riskier places may not sound like an enormous risk, but it’s rather significant. An insurance company requires substantial investment income to be profitable.

For example, in 2011, $20.362 billion of the total revenue came from premiums while $3.280 came from net investment income. There was an impairment of $1.552 billion, and $81 million in other income. When this is compared to the 2011 reported net income of $1.964 billion, it’s clear how important investment income and impairments are to the bottom line.

Realized Investment Gains (Losses) By Year, in Millions:

| Year | Gain / (Loss) |

|---|---|

| 2011 | ($1,552) |

| 2010 | ($422) |

| 2009 | ($1,212) |

| 2008 | ($1,007) |

| 2007 | $28 |

| 2006 | $79 |

| 2005 | $262 |

| 2004 | ($12) |

Gains and Losses from the portfolio were a fairly minor portion of the business until 2008 when the financial crisis began showing itself. With over $1 billion in impairments in certain years, and another $5.6 billion of PIIGS exposure on the balance sheet, this is playing a part in the current valuation. In some of these years, impairments for the year were almost as large as the net income of the company during the year.

Conclusion and Valuation

The company has particularly strong core operations but significant ongoing portfolio risks. The company seems to be taking the correct measures to de-risk their holdings, but there remains $5.6 billion in concerning debt exposure.

If the company grows EPS by 7% per year going forward, and raises the dividend by 15% per year over the next 10 years, then the dividend payout ratio will still be only 50% in ten years. If after that, they maintain a constant payout ratio, then the dividend would grow at the same pace as EPS.

Using a two stage dividend discount model, with 15% estimated dividend growth for the first 10-years and 6% terminal dividend growth, and using a 12% discount rate, I calculate that the fair price for the stock is $46. Using an 11% discount rate would yield a fair price of $56 with the same expectations of dividend growth.

Edit: I’ve made an update the to the valuation, and the above results take that update into account. The numbers are roughly the same but the discount rates are decreased by 1%.

Therefore, the current price of under $46 seems to be fairly appealing. There’s ongoing risk, and I expect the stock to have a volatile ride, but for a dividend investor with fairly high risk tolerance, I believe there is value here.

Full Disclosure: As of this writing, I have no position in AFL, though it is on my watch list for possible purchase.

You can see my stock portfolio here.

Strategic Dividend Stock Newsletter:

Sign up for the free dividend and income investing newsletter to get market updates, attractively priced stock ideas, resources, investing tips, and exclusive investing strategies:

Matt,

Phenomenal analysis. Really thorough and I think you captured the risk/reward profile with this company perfectly.

I’m personally comfortable investing with AFL at these levels and it appears to me that AFL has done a pretty solid job de-risking the bond portfolio, albeit with risks still involved. I certainly wouldn’t make AFL a core position, but there is still some solid value there to build a long-term position and collect a strong dividend stream that continues to rise well above inflation.

Best wishes!

I agree precisely.

While probably not a great core holding for most investors, it does appear to be quite a solid value pick.

Hey Matt,

Bang up job on the analysis as usual. I always learn something from your posts and never miss them. Gotta love that newsletter in my inbox on an ongoing basis.

AFL is my largest holding and though I am a bit uncomfortable with the risk angle, I take lots of risks. For example, the other day I put pickles on a peanut butter and jelly sandwich. As it turns out, that was a risky, yet incredibly rewarding move. I’m hoping AFL will follow suit.

Thanks for all that you do! I don’t always comment on your articles, but would never miss one as they’re really informative and incredibly rewarding to read. Keep it up!

Thanks for the comment, Pey.

I didn’t see you posting on Seeking Alpha for a while, but I see you’ve got some new articles after a bit of a summer break. Some editor’s picks too. :)