This article has been written by Olivier Gélinas for Dividend Monk.

Summary

- Solid business with a 47-year streak of increased dividends

- Both organic and non-organic growth are paying off for the company

- A not-so-cheap stock for an average payout

Sysco Corporation (SYY) might not be very well known by everyone, but this near dividend-king stock has benefited from nearly a 45% appreciation in their stock price. SYY dominates the food distribution industry with almost twice the sales of the second largest food distributor, US Foods (NYSE: USFD). Having now increased their dividend for 47 years consecutively, SYY might start to face some challenges in the upcoming years. Yes, the industry isn’t the easiest one, but the projected economic conjuncture doesn’t seem as shiny as it once was. Is SYY’s business model solid enough to earn you big bucks?

Understanding the Business

Sysco sells, markets, and distributes food and non-food products to restaurants, healthcare, educational facilities and lodging establishments. SYY’s customers are mostly restaurants (61%) with healthcare, education & government, and travel owning each a 9% share. The remaining 12% comes from cafeterias, bakeries and other types of stores.

SYY counts approximately 300 distributing facilities that serves their wide 500,000 customer base. In July 2017, they employed approximately 66,500 workers throughout the world.

In addition to their organic growth, the company acquired, in 2016, Cucina Lux Investments Limited, the parent holding of the Brakes Group, which they in turn, acquired during 2017. These two acquisitions complemented their supply chain in Europe and helps SYY consolidate their position in the worldwide industry.

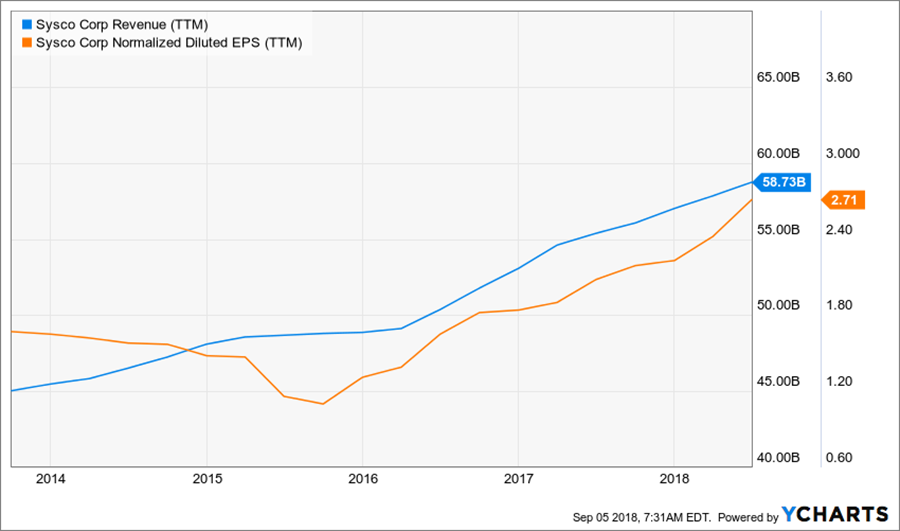

Growth Vectors

Source: Ycharts

Lately, SYY acquired 2 businesses to complement their activities in Europe. Both acquisitions seemed to have pleased investors, and I would not be surprised if SYY was looking to get further non-organic growth by acquisitions. As they said in their latest annual report, the company needs to be able to finance their acquisitions with a perfect balance of debt and equity.

Overall, SYY’s plan for growth is simple. Financing their activities in a perfectly balanced manner and a lean growth through operating income. As margins could tighten up in the upcoming quarters, having a solid business model in the background is surely a good way to go.

What their fourth quarter looked like

On August 13th, the company reported the following results:

- A $0.94 EPS, beating estimates by a shy $0.01

- Revenue of $15.32B, a 6.2% increase compared to same period last year and a $20M bump over estimates

- A steady dividend of $0.36 a share.

Tom Bené commented on Sysco’s performance:

“Overall, I am pleased with our performance in fiscal 2018, which culminated in the successful delivery of our initial three-year plan, including the achievement of our adjusted operating income growth target. As we head into fiscal 2019, we remain confident in our ability to profitably grow the business and accomplish our objectives”

Dividend Growth Perspective

SYY shows a record of 47 consecutive years of increasing annual dividends. The dividend king title is in sight for this 49-year-old company. Their history is living proof that the company manages their cash flows in a sustainable way and should be doing so in the foreseeable years.

Source: Ycharts

Dividend yield has been slowly declining for the past few years, however, reaching a level under 2%, which is pretty much in line with the industry average. Of course, this downtrend is accelerated by the stock price going through the roof. Even if dividends increase YoY, it won’t be able to catch up the earlier days yields.

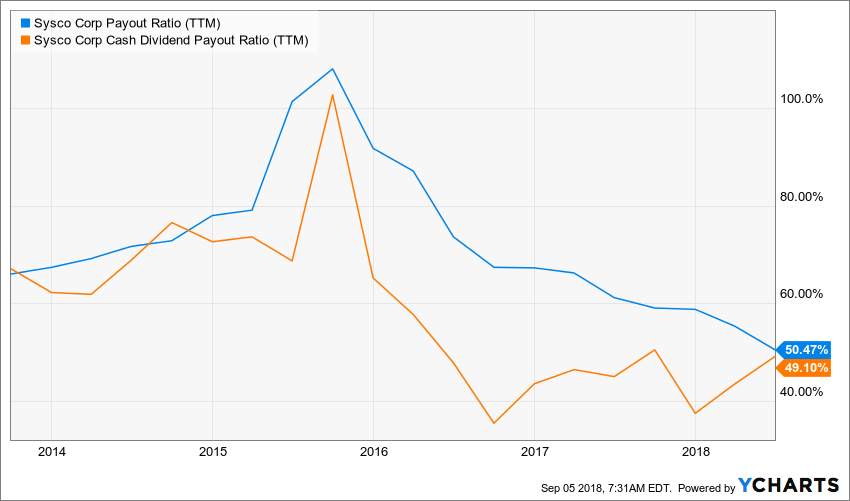

Source: Ycharts

SYY’s payout ratio of 50% shows that the company is in a healthy position at the moment. Their cash dividend payout is also nearly at 50%. This means that their net income is almost identical to their available cash. If the company does not have any more big acquisitions in mind at the moment, I would say that this payout level is sustainable. But I would be too worried if this figure dropped a bit as soon as SYY finds a potential target.

Potential Downsides

When working close to or around the food industry, margins are pretty low. Multiple restaurants are struggling to keep their business running and in good financial health. A prolonged inflation period could rapidly make prices go up. For a company like SYY, higher prices in their industry are hard to pass on customers since they are already having a hard time. Margins could be poached in order to keep their customer number up.

Another downside of this type of business, even if manageable today, resides in fuel costs. Fuel costs are going up everywhere around the globe. Yes, derivatives contracts can help diminish this growing pain, but it is still present and will also be for the next decade at least. (Or until the automotive industry makes a breakthrough. No pressure, Elon)

Valuation

SYY’s price earnings ratio is on an uptrend. But that’s mainly because of their stock price soaring in the last 2 years. Again, the company position itsself in the average of their industry. Soaring prices does make one wonder if it is still time to buy this stock.

Source: Ycharts

For this DDM, a 5% dividend growth was used for short and long run. Computing the last few dividend increases on an annual basis, a 5% level seems appropriate. A discount rate of 9% is also factored in.

| Input Descriptions for 15-Cell Matrix | INPUTS | |||

| Enter Recent Annual Dividend Payment: | $1.44 | |||

| Enter Expected Dividend Growth Rate Years 1-10: | 5% | |||

| Enter Expected Terminal Dividend Growth Rate: | 5.00% | |||

| Enter Discount Rate: | 9.00% | |||

| Discount Rate (Horizontal) | ||||

| Margin of Safety | 8.00% | 9.00% | 10.00% | |

| 20% Premium | $60.48 | $45.36 | $36.29 | |

| 10% Premium | $55.44 | $41.58 | $33.26 | |

| Intrinsic Value | $50.40 | $37.80 | $30.24 | |

| 10% Discount | $45.36 | $34.02 | $27.22 | |

| 20% Discount | $40.32 | $30.24 | $24.19 | |

Please read the Dividend Discount Model limitations to fully understand my calculations.

The model doesn’t give any output value near the $75 level we are experiencing in current markets. It is true that the company showed a lot of success by their active management and solid business model. But with those figures, I’d say the stock may be overvalued.

Final Thought

Sysco Corp. is a solid company in its industry. They showed to their investors how solid they are with an almost perfect dividend output over 47 years. Their business model and management style also seem to pay off as sales are booming and are currently way over their closest competitor.

Taking the stock by the financial metrics proves to be kind of disappointing. The stock does position itself in the average of the industry in terms of payout and PE. Their stock price just might be a little expensive for some individuals. Income-seeking investors, you should definitely look closer at this title. But if your goal is mainly in capital gain, room for upside is quite limited.

Disclosure: We do not hold SYY in our DividendStocksRock portfolios.

Leave a Reply