Yum Brands is the owner of Kentucky Fried Chicken, Taco Bell, and Pizza Hut fast food restaurants.

![]()

-Seven Year Revenue Growth Rate: 4.9%

-Seven Year EPS Growth Rate: 12.4%

-Recent Dividend Growth Rate: 17.5%

-Current Dividend Yield: 1.92%

-Balance Sheet Strength: Moderate

Overview

Yum Brands operates the brands of Kentucky Fried Chicken, Taco Bell, and Pizza hut, with over 37,000 restaurants in over 120 countries. The company was spun off from Pepsico in 1997, and maintains a partnership with that company. Although not the largest in terms of revenue, Yum Brands is the largest restaurant operator in the world in terms of the number of locations. Over three-quarters of the restaurant locations are franchises while the remaining quarter is company-owned.

While many expanding American companies still count the U.S. as their largest base of revenue and profits, this isn’t the case for Yum. China provides nearly half of their total company-wide operating profit, while the U.S. locations provide less than one third. Part of this has to do with the strength of the Chinese locations, but the other part of this has to do with the fact that Yum directly owns more locations in China. While there is a significantly larger number of KFC, Taco Bell, and Pizza hut locations in the U.S. than in China, the majority of those are franchises. But in China, Yum directly owns most of the locations, and so their revenue/operating spread is more closely centered on China than their overall restaurant count would imply.

Ratios

Price to Earnings: 20

Price to Free Cash Flow: 2.8

Price to Book: 14

Return on Equity: 77%

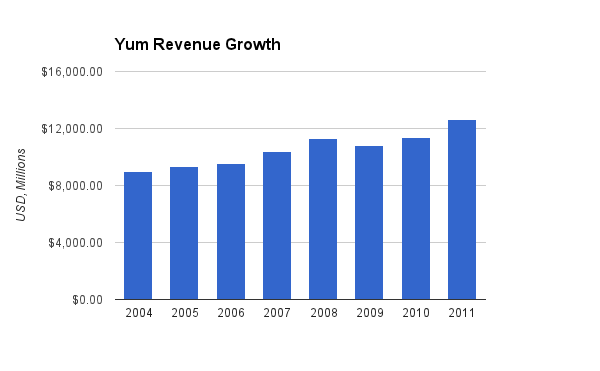

Revenue

(Chart Source: DividendMonk.com)

Revenue has grown by an average of nearly 5% per year. This solid top line growth provides a good basis for better bottom line annualized returns. Revenue is up to over $13.5 billion over the trailing twelve months.

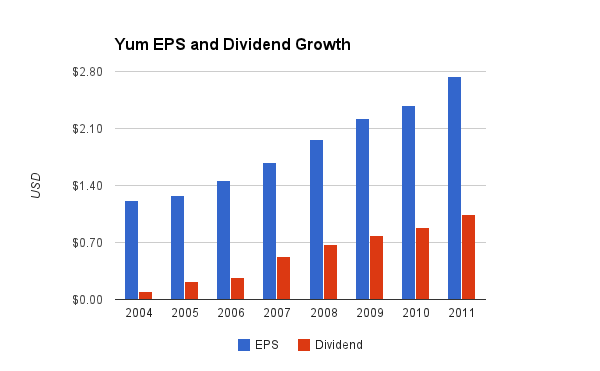

Earnings and Dividends

(Chart Source: DividendMonk.com)

Net income grew by 8.6% per year while EPS grew by 12.4% per year, with the difference being due to the share buybacks that the company has been doing.

The annualized dividend growth rate has been nearly 40% over the past seven years, but this is because the company initiated the dividend during this period and has quickly grown the payout ratio. The most recent quarterly dividend increase was 17.5%, which is still an above average figure. Over the short term, the company can quickly grow the dividend and boost the payout ratio. Over the long term, dividend growth will have to level out with EPS growth, which is currently in the low double digits.

How Does YUM Spend Its Cash?

The company generated $3 billion in free cash flow over the years of 2009, 2010, and 2011. Over this same period, the company spent over $1.2 billion on dividends and over $1.1 billion on share repurchases. In years prior to the recession during the middle of the last decade, considerably more money was spent on share repurchases to the tune of over $1 billion per year generally. The share count has been reduced by over 23% over the past decade, which has accelerated EPS growth and dividend growth above the net income baseline core growth.

A side effect of this is that the better YUM stock does, the lower the EPS growth will be, all else being equal. The company allocates cash towards buying shares, so the lower the stock price is, the more shares they can buy and the faster they can reduce the share count. The higher the share price is, the more slowly the share count is reduced. And when the valuation of the stock is in overvalued territory, the returns on investment for share repurchases are poor.

Balance Sheet

Yum has a total debt/equity ratio of over 140%, which is relatively high. Book value is fairly low compared to share price. Goodwill represents a fairly low percentage of shareholder equity.

Total debt/income, however, is under 2x. The interest coverage ratio, representing how many times over the company can pay its debt interest from operating income, is over 13x. These figures are rather conservative.

So while the company is using a significant degree of leverage and the quality of their metrics is divided, their overall balance sheet strength is on the stronger side of moderate.

Investment Thesis

Yum Brands entered the Chinese market back in the late 1980’s before it was spun off as a separate company. This early initiative that has grown over time gives it a stronger position in the country than even McDonald’s. Yum now has thousands of locations in China, with the vast majority of them being KFC units and the smaller minority being Pizza Hut locations. In 2011, 650 locations were opened, and in 2012 this looks like it’ll be around 750.

India represents a much smaller, but still significant area of growth. The number of locations remains low, but their rate of openings is the second highest of any country for Yum.

For any business that has to do with scale, reaching a certain point of critical mass can dramatically increase profitability and effectiveness. This holds true whether we’re talking restaurant locations, Wal-Mart stores, or military assets. Starting a foothold in a new region is not particularly profitable at first, because the logistics of providing the supplies are too big for the returns generated by those units. But when hundreds and eventually thousands of locations open up in a region, the logistics become robust and their scale beings to work in the favor of the business. Yum has reached this point in China, and Morningstar analysts have estimated that Yum could eventually grow its number of locations to five times the current number in China.

Probably the most interesting number presented by the company is that they have 58 locations per 1 million people in the United States, but only 2 locations per 1 million people on average in the 10 largest emerging markets. That shows how even attaining a fraction of the depth in some of these markets can mean thousands and thousands of locations.

Yum is also doing well in developed countries outside of the United States. I wouldn’t have expected it, but the company reports that their French locations have the highest per-location volume in their business. The company is in a position where it could grow its number of locations in Germany and France (currently measured in the dozens and low-hundreds, respectively), by tenfold.

So while large, Yum is still nowhere near becoming too big or running out of areas to grow. And if over a given time period, the size of the company doubles, the overall shareholder return should be much more than a doubling, because most of the free cash flow is going towards paying dividends and reducing the share count.

Acquisitions and Sales

In late 2011, Yum sold its Long John Silvers and A&W Restaurants to franchisees. This allows them to consolidate and focus their operations in the United States on KFC, Taco Bell, and Pizza hut.

In early 2012, Yum went the opposite way and acquired Little Sheep, a restaurant chain in China with around 450 locations. So they have sold assets in America to consolidate and focus, while buying assets in China to expand.

Risks

Yum’s operations in the United States have been lackluster. While the number of Chinese locations has grown considerably and the per-unit numbers are trending upwards as well, the number of U.S. locations has been roughly flat and the performance per location has been slipping. The health of the franchisee companies is poor in general.

The company has taken steps to fix this, and highlights the need to improve their results in the country. This played a role in the sale of their minor brands to focus on their big three brands. Each of those three brands has the largest market share in their category, so a turnaround is possible if the right mix of focus and strategy is used. So U.S. Yum locations represent both a risk and an opportunity. This geographic segment could eat away from expanding profits elsewhere, or the bleeding could be stopped and growth restored. While Yum brands has a greater number of overall locations than McDonald’s, McDonald’s has far larger revenue figures because their per-unit numbers are in a different league than Yum. This shows the disparity in the strength of the locations, but also shows the upside potential.

In China, the health of the business is strong, so risks appear to be more in the realm of politics and macroeconomics rather than microeconomics. The chance of poor company performance seems low at this point, but any economic recession or depression in China, or any big moves by Chinese government, could potentially disrupt these otherwise healthy operations. And unlike many U.S. companies, their investment in China is well beyond the infancy stage and into the adulthood stage, meaning any disruption in this country has enormous impacts on their overall company-wide performance.

Conclusion and Valuation

The company is currently trading for slightly over 20x earnings. Considering that China represents over 40% of Yum’s operating profits, and the operating profit from that country is currently growing at a rate that results in a doubling every 4-5 years for that region, the company as a whole seems to be have rather large growth opportunities ahead. They haven’t yet seriously tapped into India, Europe, or Africa.

The sale of the minor brands to focus on the faltering major brands in the U.S. is promising, and while poor U.S. performance remains a risk, I believe the company is well-prepared to improve it. Overall, I find the current price of around $70/share to be rather reasonable due to low double digit EPS growth and a low dividend yield added onto it. Total shareholder returns over the medium term can potentially be in the low double digits even if the stock valuation slips into the mid-high teens.

Full Disclosure: As of this writing, I have no position in YUM and am long MCD.

You can see my dividend portfolio here.

Strategic Dividend Newsletter:

Sign up for the free dividend and income investing newsletter to get market updates, attractively priced stock ideas, resources, investing tips, and exclusive investing strategies:

As always great analysis! I have been keeping my eye on YUM and as the market keeps trending downward I’m starting to glance at it more often. I know a lot of talking heads say China is about as bearish as you can get right now. With that said I may pull the trigger on YUM brands sooner rather than later. I’ll most likely try and scale into my position.

Most economies are bearish right now.

Generally I try to hold assets everywhere so that if one area does better than expected and one area does worse than expected, the portfolio lands somewhere in the middle.

Thanks for writing about Yum. I have held shares for a few years and you have made compelling reasons for them to continue to grow. Do you think eventually you might buy in? Thanks

It’s great to see the continually amazing posts Matt. And you sure are right about Yum brands. Throughout SE Asia (I live in Singapore and travel a lot) their restaurants are prolific, packed, and popping up everywhere!

Hi Andrew,

Nice to see you around again, and thanks for the description of how things are in the first person for Yum in SE Asia. It’s always good to see a comment here or on Seeking Alpha when people are in a position to talk qualitatively about something I am only in a position to discuss quantitatively.