-Seven Year Revenue Growth Rate: 5.6% ![]()

-Seven Year EPS Growth Rate: 7%

-Seven Year Dividend Growth Rate: 15%

-Current Dividend Yield: 2.08%

-Balance Sheet Strength: Very Strong

Medtronic looks solid in the mid-$50’s, but not with a margin of safety. Looking for dips or writing puts would be a more conservative approach.

Overview

Founded in 1949, Medtronic, Inc. (NYSE: MDT) is a medical technology company focusing on alleviating pain, restoring health, and extending life for people all over the world. With over 46,000 employees and a market capitalization of over $50 billion, Medtronic is the world’s largest independent medical device company.

Approximately 45% percent of company revenue comes from outside of the United States. The company markets its products in over 120 countries.

The company is divided into two primary groups.

Cardiac and Vascular Group

Medtronic’s core area of expertise has long been the heart and related systems, and slightly more than half of total company sales come from this group. The group contains four segments:

Cardiac Rhythm Disease Management

This segment accounts for 30% of total company sales. Products in this segment include pacemakers, implantable defibrillators, leads and delivery systems, ablation products, electrophysiology catheters, and other products.

Coronary, Structural Heart, and Endovascular

These other three heart segments account for 11%, 7%, and 5% of total company sales.

Restorative Therapies Group

Medtronic has been growing their products for ailments unrelated to the heart since the 1990’s, and now they collectively represent nearly half of company sales.

Spinal

This segment accounts for 19% of total company sales. Products in this segment include thoracolumbar, cervical, neuromonitoring, surgical access, and more.

Neuromodulation

This segment accounts for 11% of total company sales. Products include implantable systems for treatment of chronic pain, movement disorders, bladder problems, and other conditions.

Diabetes

This segment accounts for 9% of total sales. Products include insulin pumps and disposable products.

Surgical Technologies

This segment accounts for 9% of total sales. Products of this segment are used to treat ear, nose, and throat conditions.

Ratios

Price to Earnings: 15.4

Price to Free Cash Flow: 13.4

Price to Book: 2.9

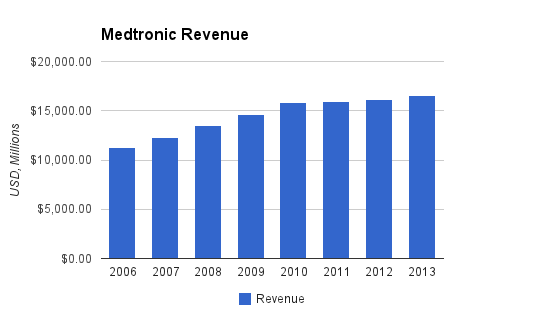

Revenue

(Chart Source: DividendMonk.com)

Revenue growth was a solid average of 5.6% per year over this period. It’s consistent as well- looking back over a decade there have not been any years where revenue fell compared to the previous year.

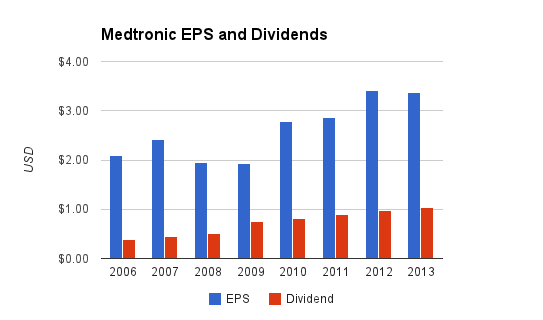

Earnings and Dividends

(Chart Source: DividendMonk.com)

Growth of EPS per share was fairly mediocre, at 7% per year on average. The growth was rather erratic as shown on the chart, but this was due to reasons other than core profitability from sales. Multiple variables of litigation costs, acquisition-related items, and restructuring charges, were involved each year. For example, the low figure of 2009 was due to a combination of substantial litigation and acquisition-related items.

Those costs are part of doing business, but factoring them out to get a different look at profitability shows that, if those types of costs are factored out, EPS grew each year over this period compared to the previous year.

The dividend growth rate over the same period averaged 15% per year, because the company wisely decided to increase its payout ratio from under 20% to currently just over 30%. The current yield is still fairly low at 2.08%, and the company has three and a half decades of consecutive annual dividend growth without a miss.

Approximate historical dividend yield at beginning of each year:

| Year | Yield |

|---|---|

| Current | 2.1% |

| 2013 | 2.4% |

| 2012 | 2.5% |

| 2011 | 2.4% |

| 2010 | 1.8% |

| 2009 | 2.3% |

| 2008 | 1.0% |

| 2007 | 0.8% |

| 2006 | 0.7% |

How Does Medtronic Spend Its Cash?

Over the fiscal years of 2011, 2012, and 2013, Medtronic brought in $11.6 billion in cumulative free cash flow. Over the same period, $3 billion was spent on dividends, $3.8 billion was spent on share repurchases, and $2.3 billion was spent on net acquisitions.

Balance Sheet

The total debt/equity ratio of the company is about 60%. Of the nearly $19 billion in existing shareholder equity, over $10 billion of that is goodwill.

Total debt/income is a bit over 3x, and the interest coverage ratio is nearly 30, which is extremely healthy.

Investment Thesis

A considerable portion of the total Medtronic offer of shareholder returns comes from dividends and buybacks. The second major portion comes from expanding the business with small and medium acquisitions and research and development of more advanced products in developed markets. The third key portion is to expand their platform to less developed areas that may be considered roughly developed, but aren’t nearly at the same level of health care spending as some of the most developed areas.

Dividends and Buybacks

The shareholder yield of Medtronic tends to be about 4-5% per year, which represents a fairly reliable portion of returns over the long term; dividends are immediate and buybacks increase EPS. Add onto that perhaps 2% top line pricing growth each year to keep up with inflation which boosts revenue and income, and the result is that 6-7% of total returns come before actual company growth. Growth adds onto that foundation of returns to get us up to where we want to be at around 10% annual returns or better, so before core growth is even factored in we’re already two-thirds of the way there (a reminder of the virtue of a good dividend stock, even if Medtronic’s yield is at least 1% lower than I’d like).

Research, Development, and Acquisitions

Medtronic spends about $1.5 billion, or roughly 3% of market cap, on R&D each year. This includes new and improved medical devices, such as new products to treat conditions, updates on existing products for increased effectiveness or increased longevity, or updates on existing products to make them resistant to the effects of MRI scans. Major pipeline projects for fiscal year 2014 include the RestoreSensor SureScan MRI spinal cord system, the MiniMed 530g/640g diabetes systems, and the Endurant II AAA stent graft.

Acquisitions by their nature tend to be more erratic, but it’s not uncommon for Medtronic to spend 2% or more of its market cap on acquisitions in a given year. The Aquamantys system, acquired in 2011, uses a combination of RF technology and a saline to reduce blood loss during surgery. The PEAK PlasmaBlade is a scalpel that uses pulsed plasma technology. A typical scalpel cuts but causes significant blood loss, so an alternative is to do electrosurgery which uses electrical current to produce heat and cut tissue, which reduces blood loss but can cause thermal damage. Pulsed plasma technology is reported to do less thermal damage than electrosurgery while maintaining satisfactory blood loss control.

Market Expansion

Medtronic continues to invest and expand into markets with the idea that they should pay well in the future. In particular, Medtronic makes acquisitions and expands treatment options into China each year, so that they can establish a strong platform in the country as it grows per-capita GDP and health care costs.

Risks

Like all large health care companies, Medtronic faces considerable litigation and regulatory risk. As mentioned in the EPS section, EPS can be materially affected by litigation costs alone. There’s also regulatory risk, which can delay or disrupt large product introductions.

A major industry risk is that health care costs, especially in the United States, are considered by many to be out of control. The United States is the third most populated country in the world and has by far the highest per capita health care costs, but this is breaking both the federal budget and the budgets of middle class workers and their employers attempting to provide health care benefits to them. Any reductions in health care spending to try to reign in health care costs may impact medical devices, with Medtronic being the largest industry player.

Conclusion and Valuation

With consistent revenue growth, a very strong balance sheet, a long history of dividend growth, and a mediocre current dividend yield, Medtronic can be a decent health care selection for a portfolio.

Based on the Gordon Growth Model using a 10% discount rate (target rate of return), if Medtronic grows its dividend by an average of 8% per year for the foreseeable future, then the calculated fair value is a bit over $57. The current price is about $54. However, the most recent dividend increase was a bit under 8%, and if the average projected dividend growth rate drops to even 7.5%, then we’re looking at a fair value of more like $45. The model is sensitive for lower yield stocks, and there isn’t really a margin of safety here.

Another path is to hold off for dips, or write put options on the stock at a strike price about where the price is now. The February 2014 contracts at a strike price of $52.50 aren’t bad (results in a cost basis of about $50 if exercised), and for a longer term idea, the January 2015 contracts at a strike price of $55 potentially offer a decent annualized rate of return with a current cost basis of a bit below $49.

Full Disclosure: As of this writing, I am long MDT.

You can see my dividend portfolio here.

Strategic Dividend Newsletter:

Sign up for the free dividend and income investing newsletter to get market updates, attractively priced stock ideas, resources, investing tips, and exclusive investing strategies:

Simply outstanding details…but I’m not surprised anymore :)

I don’t own MDT but would like to. With an aging population, this is the sector to be in for the next 30 years.

Mark

I’m no longer positive where you are getting your information,

however great topic. I needs to spend some time finding out more or figuring out more.

Thanks for magnificent info I was on the lookout for this

information for my mission.