McDonald’s Corporation is one of the most well-known companies in the world, and the largest restaurant chain by revenue.

-Seven Year Revenue Growth Rate: 4.4%![]()

-Seven Year EPS Growth Rate: 14.8%

-Seven Year Dividend Growth Rate: 23%

-Current Dividend Yield: 3.14%

-Balance Sheet: Strong

At the current price of under $100, I view McDonald’s as being rather attractively valued as a dividend growth stock.

Overview

McDonald’s Corporation (NYSE: MCD) was founded by the McDonald brothers, but it was the early partner Ray Kroc that expanded McDonald’s into the company it is today. The brothers wanted a small set of restaurants, and Kroc wanted to expand, which led to Kroc buy the company from the brothers. His vision built the company into the largest restaurant business in terms of revenue, and in many McDonald’s corporate statements, Kroc is called a “founder”.

McDonald’s has been in business since 1940, and has been raising their annual dividend consecutively since the mid 1970’s. The company has restaurants all throughout North and South America, Europe, Australia and Asia, but are only thinly available in the Middle East and Africa. The primary food products they serve are hamburgers, cheeseburgers, chicken meals, french fries, coffee and milkshakes, but they are beginning to offer products like wraps, salads, and smoothies.

McDonald’s serves 69 million customers each day, which is greater than the population of countries such as France, the UK, Italy, South Korea, Canada, and Thailand. As of the end of 2012, the company operates in 119 countries and has 34,480 restaurants, with around 80% being franchised or licensed businesses and the other 20% being company-owned. In 2012, 970 net new restaurants were opened. This included 1,439 openings and 469 closings.

The franchisee owned restaurants have higher profit margins than the corporate owned restaurants (McDonald’s collects rent and royalties), but the corporate owned restaurants allow McDonald’s to develop new products and new looks and keep management teams knowledgeable and well-trained.

In terms of geography, 32% of McDonald’s revenue comes from North America, 39% comes from Europe, and 29% comes from elsewhere.

New CEO

A year ago, Don Thompson took over the CEO reins from Jim Skinner. Thompson originally joined the company in 1990 as an electrical engineer, and rose through the ranks to become a regional vice president and eventually the COO and now the CEO.

McDonald’s maintains a separate chairman of the board from the CEO, which can allow for improved oversight of the board to the management team. McDonald’s managers, from the senior vice presidents, are expected to own at least 2x to 6x as much McDonald’s stock as their base salary; 2x or 3x for the SVPs, 4x or 5x for over executives, and 6x for the CEO.

Ratios

Price to Earnings: 18

Price to Free Cash Flow: 25

Price to Book: 6.5

Return on Equity: 36%

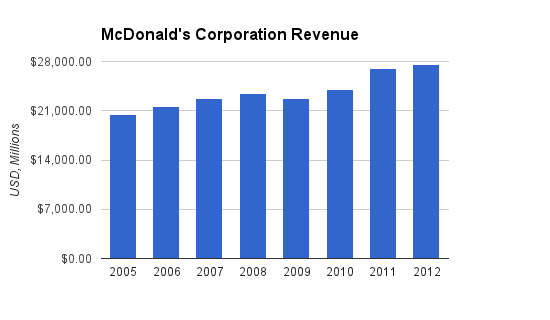

Revenue

(Chart Source: DividendMonk.com)

Revenue grew at an average rate of 4.4% per year over this seven year period.

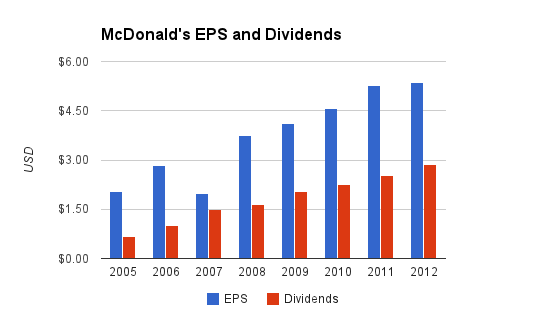

EPS and Dividends

(Chart Source: DividendMonk.com)

EPS grew by an annualized rate of 14.8%. The dividend growth rate over the same period grew by 23%. These are strong values that should not be expected for the future; the dividend payout ratio increased over the period but must eventually keep in line with EPS growth, and future EPS growth itself will almost certainly be lower than this period.

The dividend yield is currently 3.14%, and the dividend payout ratio from earnings is approximately 55%.

Approximate historical dividend yield at beginning of each year:

| Year | Yield |

|---|---|

| Current | 3.14% |

| 2013 | 3.4% |

| 2012 | 2.8% |

| 2011 | 3.3% |

| 2010 | 3.5% |

| 2009 | 3.2% |

| 2008 | 2.6% |

| 2007 | 2.3% |

| 2006 | 2.0% |

How Does McDonald’s Spend its Cash?

For the fiscal years 2010, 2011, and 2012, McDonald’s brought in a cumulative $12.5 billion in free cash. Over the same period, $8.6 billion was spent on share buybacks, $7.9 billion was spent on dividends, and the company had a net acquisition profit. The company has reduced the outstanding share count by approximately 20% over the last decade.

The shareholder yield of the company is typically over 5% per year.

Balance Sheet

McDonald’s has a debt/equity ratio of about 85%, and less than 20% of the existing shareholder equity consists of goodwill.

The debt/income ratio is 2.4x, and the interest coverage ratio is over 16x. Overall, McDonald’s does use a moderate amount of leverage, but the balance sheet is extremely strong and the company maintains above average credit ratings.

Investment Thesis

As global business, there are numerous variables that drive McDonald’s profitable growth.

Franchisee Expertise and Prime Locations

We are in the real estate business, not the hamburger business.

-Ray Kroc

As a general rule, the typical McDonald’s location brings in substantially more customers and revenue than other fast food branded locations. This is partly because ever since the involvement of Ray Kroc, real estate has been a major focus of the company. While Pizza Hut or Wendy’s locations may often be in less ideal locations, McDonald’s generally benefits by being a first-mover in an area, or goes to the extra expense of securing the best location. Although not all of their locations meet this target, their ideal spot that they aim for is a corner location on the intersection of two major streets with traffic signals, and the company often owns the land and the building or has a very long term lease.

In addition, franchise owners of McDonald’s locations are particularly well trained. First, a potential franchisee must generally have $750,000+ in non-borrowed assets exclusive of their home to pay for a down payment. Larger business entities can operate multiple locations. Secondly, owners and managers attend Hamburger University. This is McDonald’s 130,000 square foot facility with 19 full-time instructors. Over 5,000 students attend each year, and since 1961 80,000 students have graduated.

The result of this is that McDonald’s does very well on a per-restaurant basis, and the turnover rate is very low. Well under 1.5% of McDonald’s locations close each year. Under-performing restaurant locations can harm the brand, so McDonald’s takes each location seriously and only moves forward if there is a strong calculated chance for long-term success.

Focus

MCD has been selling various investments in order to focus on the McDonald’s brand. They performed an initial public offering of Chipolte Mexican Grill in 2006, sold Boston Market in 2007, and sold Pret A Manger in 2008. The focus has been placed on the McDonald’s brand, which is revitalizing its image and introducing new products. The company has been remodeling their restaurants worldwide to include softer colors and more wood to replace the red and yellow plastic look, and has since remodeled 60% of interiors and expects to have remodeled 50% of exteriors by 2015 according to the 2012 annual report. Many of the remodeled locations had drive-through systems added in order to expand the customer base.

McDonald’s McCafe brand now has over 1,600 locations. McCafe can be combined with McDonald’s locations, but also can be put in new areas to enter new markets and reach new people.

McDonald’s spent three quarters of a billion dollars for advertising in 2012. The company’s size and focus allows it to outspend its rivals; smaller rivals don’t have the budget to advertise to nearly the scale of McDonald’s, and large rival Yum Brands must split their significant advertising budget into KFC, Taco Bell, and Pizza Hut.

Comparable Growth

The key metrics to watch with McDonald’s are guest count and comparable sales for their existing locations. It’s not that difficult for McDonald’s to continue to open new restaurants around the world, but it’s challenging to do that while also growing or maintaining the guest count and sales of their existing locations, on average. In 2012, average guest count was up 1.6% and comparable sales were up 3.1% according to the latest annual report. The 2012 figures for the United States are slightly stronger, and in fact the company has increased comparable sales in the country for ten consecutive years.

Profit Margins

The profit margins of McDonald’s are above competitors, which is evidence of a strong competitive advantage. MCD’s net profit margin is over 20%, which is almost double that of competitors such as Starbucks and Yum! Brands, and considerably higher than businesses like Dunkin Donuts or Wendy’s. Some of this has to do with their heavy focus on franchises; franchises produce better profit margins than company-owned restaurants. But some of this also has to do with superior performance per location; their sales figures per location are considerably above their peers, and their profit margins are quite high even on their company-operated restaurants. Most of the growth of the company is due to organic growth, which results in little goodwill piling up on the balance sheet, and means the free cash flow can be given back to shareholders.

Risks

McDonald’s faces the usual currency, litigation, and geographic catastrophe risks associated with all global businesses. Commodity cost changes have a meaningful impact on profitability as well.

The company has a rather defensive business, as evidenced by their strong performance through the recession and tough global economic times, but they still must continually stay relevant among consumers. The company is in the midst of a considerable modernization program for their restaurants, which shows their ability to identify and change along with trends.

Politics could present a risk, as much of the company’s food materials supplied by farmers are directly or indirectly federally subsidized. The company does have considerable pricing power over its suppliers, though. In addition, food items targeted for potentially contributing to national health problems could face taxes, bans, or simply changing consumer interest, and with McDonald’s visibility, they tend to face a considerable portion of criticism.

Conclusion and Valuation

McDonald’s continues to maintain a fierce position in a competitive industry. Their size and unrivaled advertising budget, along with popular new menu items, drove solid comparable results for the existing restaurants. Their properties are of high value, and their management teams are among the most highly trained, and their balance sheet is rather strong.

The company aims for 3-5% long-term system-wide annual sales growth and 6-7% annual operating income growth. An expected 1,500 new locations are expected to be opened by the end of 2013 compared to the end of 2012. If the company can continue to hold solid sales growth on existing locations, continues to open over a thousand new locations each year, and continues to use the profit to pay dividends and buy back shares, then McDonald’s should be able to deliver shareholders robust, diverse, and defensive returns.

McDonald’s dividend growth rate has been very high in the past, and the company has decades of consecutive annual increases without a miss. I believe that a fairly conservative estimate for the long-term dividend growth rate is at least 7%, based on a stable payout ratio from EPS. Their EPS can fairly easily grow by 7+% per year driven by 4% annual sales growth, 3% of the market cap in buybacks per year, and static profit margins.

Based on the Gordon Growth Model using a 10% discount rate, if McDonald’s long-term dividend growth rate is 7% per year, then the fair stock price is $107.

Therefore, I believe that the stock price at just over $98 is reasonably appealing at the current time.

Full Disclosure: As of this writing, I am long MCD.

You can see my dividend portfolio here.

Dividend Stock Newsletter:

Sign up for the free dividend investing newsletter to get market updates, attractively priced stock ideas, resources, investing tips, and exclusive investing strategies:

Nice analysis. An additional point is that the company is accelerating its expansion in China, planning to hire an additional 75,000 workers this year (an 83% increase) and opening 300 more outlets (for a total of 2,000 on mainland China). The company has about 16% share of China’s fast-food industry (compared with 39% for Yum Brands), so this could be a strong driver of growth over the next several years.

Although I am also a McDonald’s shareholder, I did not know the story of the McDonald brothers and Ray Kroc. Thanks for sharing that! I love companies with high margins. As you point out, it is a strong indicator of a competitive advantage.

I recently bought MCD (but I paid more than $100 :-( ). I think the stock will continue to go up as the global economy hasn’t pick-up yet. I strongly think MCD is the kind of stock to hold in your book forever.

cheers,

Mike

OK, I must admit I didn’t know about the property strategy of MCD and when looking back to locations I had a chance to visit worldwide this makes totally sense and they truly were trying to pick the best locations. Whenever we wanted a fast food wherever we were, it was always (magically) MCD we were able to spot first.

The Hamburger University is totally gorgeous and i wish I could attend, just for curiosity.

oh, btw, I bought MCD when it was at 86 a share, so I am well positioned. Now I am waiting if it ever gets that low again and buy more (or at least close to 90 a share). From the TA perspective there is a good chance the stock can go to a 90 – 94 range (a long term trend support line on the lower line and 200 day MA as a resistance (if the stock breaks below it). But if it ever happens and when, who knows.

This is a great dividend growth stock that could be bought under $95 if you are patient; I am still waiting for the right entry point. Price to earnings multiple <18, 3% dividend yield, 5-7% top line revenue growth, can't go wrong. Here are some interesting facts courtesy of http://www.2topdividendpayingstocks.com/mcdonalds-dividend-analysis.html

McDonalds is truly a global competitive brand with an average of 69 million customers visiting its stores every single day in over 120 countries. The company’s revenue breakdown comes from 32% (US), 39% (Europe) and 23% (Asia, Middle East and Africa). The company grew its comparable same store sales at an average of 3.1% in fiscal 2012.

For dividend growth stocks such as McDonalds, I like to see stable Return on Equity (ROE) over the past decade. Return on Equity is a measure of net income divided by shareholder's equity and shows if the firm is efficiently able to generate profits from every common stock held by shareholders. Note the company has been able to steadily grow its ROE from 12.28% in 2003 to 35.73% in 2012; except for a decline in 2007 when ROE was 15.67%. This decline is due to the company taking a pre-tax operating charge of $1.7 billion related to impairment as a result of sale of its businesses in 18 Latin American and Caribbean countries.

I really like Mcdonalds, but would like to see them around $80/share. I think we can all agree that it is a fantastic business that rewards shareholders dearly.

Everything is very open with a clear clarification of the issues.

It was truly informative. Your site is useful.

Many thanks for sharing!