Here is the 2024 Dividend Kings list and my top 5 among them for this year. Dividend Kings are companies that have been showing the longest streaks of dividend increases in stock market history. In fact, they show more than 50 consecutive years with a dividend increase. To be part of this list, the Dividend Kings must show an incredible ability to adapt their business model and constantly innovate to stay relevant and in the game. This is a great example of stability and growth in times of pandemic!

Being in business for over half a century is already hard enough. These companies are not only surviving, but they are thriving and sharing the wealth with shareholders. Investors who were wise enough to buy them decades ago have enjoyed both strong capital appreciation and constant dividend growth. This article covers the following topics regarding the Dividend Kings (click on the title of each to jump directly to this section):

How to Calculate Dividend Kings Valuation

What Are Dividend Kings?

As mentioned in our introduction, to be named a Dividend King a company must have increased its dividend successfully for at least 50 years. Do not confuse this with 50 years of consecutive payments. There are no other restrictions to be part of this elite list. I guess completing 5 decades of dividend growth is hard enough!

As of 2024, we count 54 Dividend Kings, all of which are trading on the U.S. stock market. Two of them are Canadian companies that trade on the U.S. market but also on the Toronto Stock Exchange (TSX). Please note some Kings aren’t part of the Dividend Aristocrats list since the Aristocrat list includes only companies trading on the S&P 500.

You will find many “old consumer staples” and industrials among this list. However, you will not find stocks in the energy or technology sectors. You can bet many future dividend kings will eventually come from the tech sector.

The 2024 Dividend Kings List

A * denotes new Dividend Kings, making the list this year.

Basic Materials

Stepan (SCL)

H.B. Fuller (FUL)

Nucor Corp. (NUE)

PPG Industries (PPG)

RPM International (RPM)*

Consumer Cyclical

Genuine Parts Company (GPC)

Lowe’s Companies (LOW)

Leggett & Platt, Inc. (LEG)

Consumer Defensive

Archer Daniels Midland Co. (ADM)*

The Colgate-Palmolive Company (CL)

Hormel Foods Corporation (HRL)

Kenvue (KVUE)* after spin-off from JNJ

Kimberly-Clark Corp. (KMP)

The Coca-Cola Company (KO)

Lancaster Colony (LANC)

Altria Group (MO)

PepsiCo Inc (PEP)

Procter & Gamble (PG)

Target Corp (TGT)

Tootsie Roll Industries, Inc. (TR)

Sysco Corporation (SYY)

Universal Corp. (UVV)

Walmart Inc. (WMT)*

Energy

National Fuel Gas Co. (NFG)

Financial Services

Commerce Bancshares (CBSH)

Cincinnati Financial (CINF)

Farmers & Merchants Bancorp (FMCB)

S&P Global Inc. (SPGI)*

United Bankshares Inc. (UBSI)*

Healthcare

Abbvie Inc (ABBV)

Abbott Laboratories (ABT)

Becton, Dickinson And Co. (BDX)

Johnson & Johnson (JNJ)

Industrial

ABM Industries (ABM)

Dover Corporation (DOV)

Emerson Electric (EMR)

Gorman-Rupp Company (GRC)

W.W. Grainger Inc. (GWW)

Illinois Tool Works, Inc. (ITW)

3M Company (MMM)

MSA Safety Inc (MSA)

Nordson (NDSN)

Parker Hannifin (PH)

Stanley Black & Decker (SWK)

Tennant Co. (TNC)

Real Estate

Federal Realty Investment Trust (FRT)

Utilities

American States Water (AWR)

Black Hills Corporation (BKH)

Canadian Utilities Ltd. (CDUAF) (CU.TO… it’s a Canadian stock)

California Water Service (CWT)

Fortis Inc (FTS) (FTS.TO…another Canadian stock)

Middlesex Water Co. (MSEX)

Northwest Natural Gas (NWN)

SJW Group (SJW)

Technology

none

How to Calculate Dividend Kings Valuation

The most classic way you can evaluate dividend kings is by using the earnings multiple valuation approach, also known as P/E ratio. If you do a bit of research, you’ll notice that not all kings are trading at a good valuation right now. Many of them show P/E ratios over 15-16 which is considered the S&P 500 long-term average. After all, there is a price to pay for quality!

Another more useful way to determine which Dividend King is the best investment now is to use the dividend discount model (DDM). The DDM is used to determine the intrinsic value of a stock based on a future series of dividends that grow at a constant rate. When you look at companies with 50+ years dividend increase streaks, you can certainly use this model to assess their fair value. Please read the Dividend Discount Model limitations before making any assumptions.

You can use this free DDM spreadsheet for your calculations.

I know how hard it is to invest when stocks don’t seem to trade at their fair value

Don’t you hate not knowing when to buy or sell stocks? Too many investing articles contradict one another. This creates confusion and leaves you with the impression you will not reach financial independence. It doesn’t have to be this way. I’ve built a free recession-proof portfolio workbook which gives you the actionable tools you need to invest with confidence and reach financial freedom.

This workbook is a guide to help you achieve three things:

- Invest with conviction and address directly your buy/sell questions.

- Build and manage your portfolio through difficult times.

- Enjoy your retirement.

Top 5 Dividend Kings 2024

Here’s a quick list of my favorite long-term dividend growth companies along with their dividend triangle trend (revenue, earnings per share, dividend for 5 years), my investment thesis and potential risks.

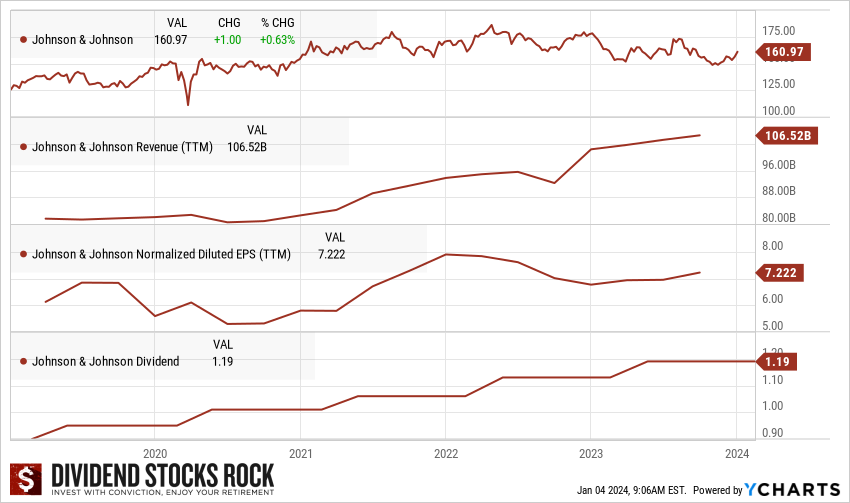

#5 Johnson & Johnson (JNJ)

Investment Thesis

JNJ is a powerful engine that is continuously being fueled to perform better and better. An investment in JNJ is an investment in a world-class company that offers a complete brand portfolio with winning products. The company is well diversified among its product offerings. Despite its relatively low yield, the company will not only reward investors with a constant and increasing dividend, but also with steady capital appreciation. We like that JNJ decided to spin-off its consumer health segment into Kenvue (KVUE). It will allow a better focus on pharmaceutical business activities and avoid confusion for investors thinking they are buying a consumer staple stock. We think JNJ’s Pharma segment continues to offer a promising outlook due to strong prospects on existing key drugs such as Stelara, Imbruvica, and Darzalex, along with a robust drug pipeline of 14 novel drugs with launches expected by end of 2023.

Potential Risks

In 2012, JNJ had several quality control issues, which affected sales and potentially hurt some of its brands. Potential lawsuits due to product defects or severe drug side effects could also impact JNJ; the company has had to handle opioid and talc powder related lawsuits. In January of 2023, an appeals court ruled against the pharmaceuticals giant in a talc case covering more than 40,000 lawsuits. The lawsuit saga is coming close to an end after JNJ won close to 75% of the over 40 talc cases that have rulings and close to two-thirds of claimants favoring the $8.9 billion settlement.

JNJ will face generic competition for many of its drugs, such as Remicade (which currently has two competitors), the cancer-fighting drug Zytiga, and HIV drug Prezista. Sales of lymphoma drug Imbruvica struggled in the US in 2022 because of competitive offerings, and margins have struggled across all segments. Increased pressure on drug pricing can also become a concern.

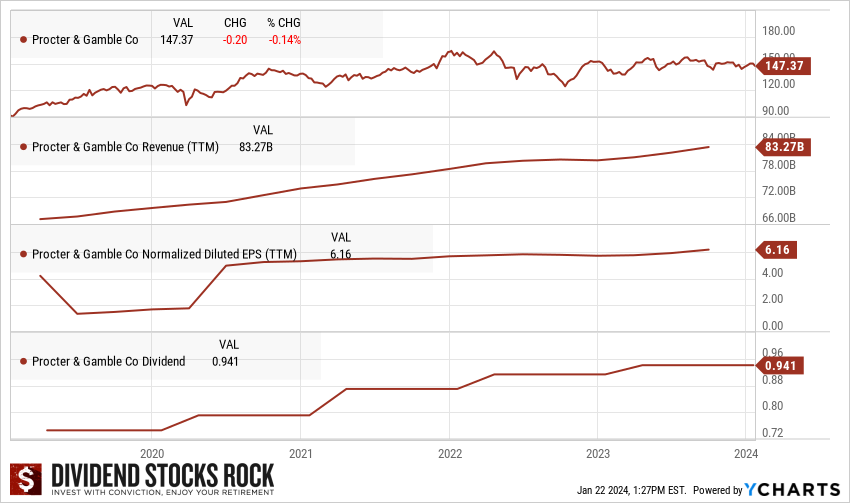

#4 Procter & Gamble (PG)

Investment Thesis

If an investor buys shares of PG, the goal should be to earn a steady and increasing flow of income. Procter & Gamble is probably more stable than most bonds and pays a decent yield. There are no immediate threats that come to mind that will jeopardize its dividend in the future. PG is a strong stock to hold, regardless of how much one pays for it. The company successfully trimmed its brand portfolio. Don’t expect a huge price appreciation here, but as the market ebbs and flows, PG is a company that will steadily continue paying its dues, even in a recession. Thanks to its best-in-class supply chain and pricing power, PG is doing relatively well, even in challenging times. This is enough to beat inflation and keep it as a long-term hold in your portfolio.

Potential Risks

While PG was focused on diversifying its product mix, it lost market share and sales opportunities in emerging markets. Smaller companies were faster and more agile in adapting to emerging markets’ needs. Now that PG is ready to take on these markets, it will require substantial sums of cash invested in marketing. Expect management to continue its cost-cutting plan, even if it will be hard to rationalize a spending increase on marketing at the same time; this is a common dilemma faced by large corporations. PG won’t be able to cut costs for many consecutive years, particularly in today’s inflationary environment. Finally, PG did well during the pandemic, but now must face a potential recession and high inflation, inviting customers to revise their budgets.

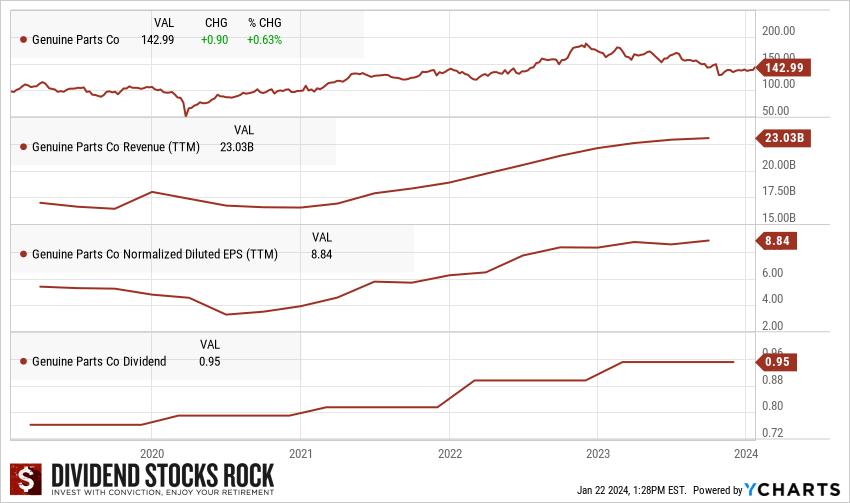

#3 Genuine Parts (GPC)

Investment Thesis

Over the years, GPC has built a solid reputation through high-level service and high-quality parts. 75% of its auto parts sales come from the commercial segment (garages). This segment lends itself to highly consistent order patterns. Genuine Parts is also known for its never-ending appetite when it comes to buying out its competitors. A winning strategy for any portfolio building method is to pick strong companies with established business models that have become leaders in their industry. GPC shows constant revenue growth and keeps its focus on productivity. This is how GPC increases its EPS faster than its revenue. GPC is the parent company of NAPA Auto Parts, which is a great performer in recessionary environments. We expect growth to be driven by an increasing U.S. vehicle age, which rose to a record high of 12.1 years in 2021. GPC is a great example of a company able to generate both organic growth and growth by acquisition.

Potential Risks

Because GPC operates in a cyclical market, some investors may get nervous when the economy slows down over the coming quarters. The auto industry isn’t growing, but automobiles continue to require maintenance. GPC’s primary source of growth is through acquisitions. The more companies they buy, the more expensive those purchases become. This dynamic may reduce GPC’s profitability on future investments. It has become difficult to acquire smaller competitors in the U.S. for that reason. Genuine Parts is now pursuing new acquisitions in the European market. We saw in the latest quarters that while it provides additional growth, GPC is now more exposed to currency fluctuation headwinds. This is a whole new game, and we don’t know if management can replicate their previous successes on another continent.

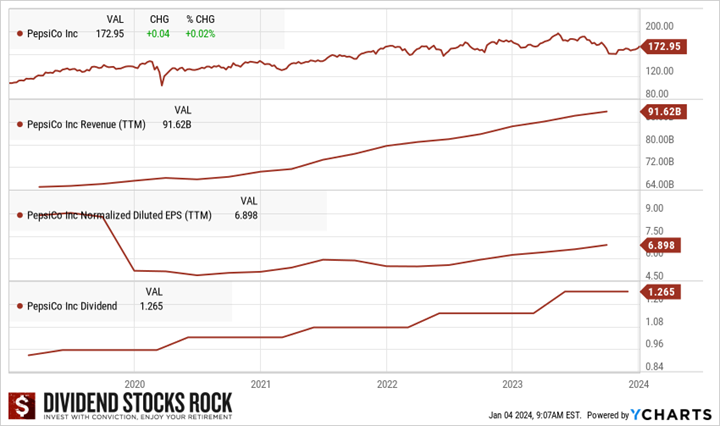

#2 PepsiCo (PEP)

Investment Thesis

While carbonated drink sales are slowing in developed markets due to health consciousness, PepsiCo benefits from strong non-carbonated drink brands such as Gatorade and Tropicana. PEP’s snack division is a strong leader in this industry, with a 64% market share in the U.S., 60% of Brazil’s market, and 46% of the U.K. market. More importantly, the 2nd place in salty snacks is far behind PEP in terms of market share and sales volume. The company is looking to consolidate its distribution for its two divisions to improve.

PEP might be one of the best stock picks when considering blue-chip defensive stocks with strong balance sheets. Throughout 2022, the company demonstrated resilience and continues to do so 2023. PEP’s focus on healthier snacks and beverages will likely continue to drive the top line. Finally, we still see a lot of growth potential in international markets and the Frito-Lay business. The big news hurting the stock price in fall of 2023 is related to the rise of weight loss drugs such as Ozempic, which could put pressure on snacks and soft drink sales. At the same time, management revised its EPS guidance for 2023 and now expects it to grow by 13% instead of 12%.

Potential Risks

Management seems to act decisively in the ever-evolving snack foods market, but where are the future growth vectors with such rivalries? PEP’s small initiatives (like developing portable breakfasts) do not seem to be enough to support strong growth moving forward. The Snack division saved its seat, but competition is on the rise. Companies like Hershey are eyeing the snack and breakfast markets for expansion. Although PEP benefits from strong brand recognition and solid relationships, this does not completely solve the problem. After all, PEP is still the eternal 2nd behind Coke in the beverage industry. Finally, the rise of weight loss drugs such as Ozempic is making the news and the market is concerned it will impact snacks and soft drink (along with other “unhealthy” food options) going forward.

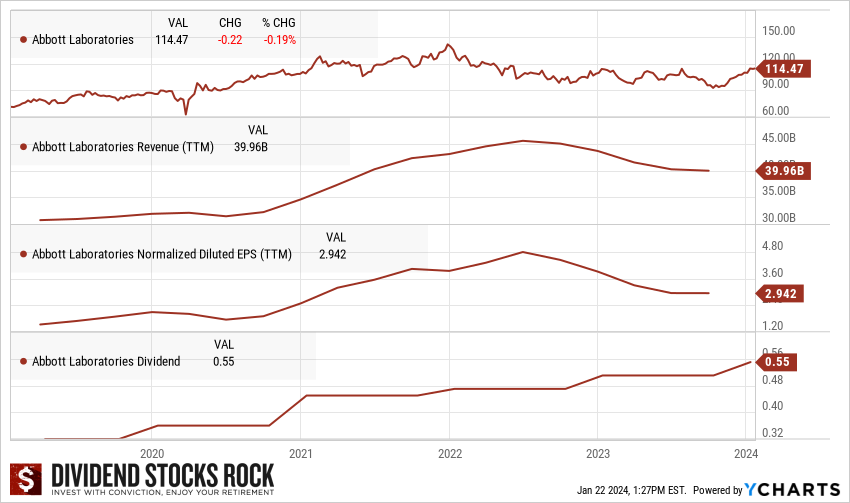

#1 Abbott Laboratories (ABT)

Investment Thesis

After spinning off its research-based activities into AbbVie (ABBV) several years ago, ABT now focuses on various medical devices, nutritional products, and branded generic medicine distribution. Its major acquisitions in 2014 and 2017 strengthened the company and created numerous growth vectors for years to follow. ABT has successfully integrated St. Jude Medical, which opened the door to the structural heart product industry. ABT has a long history of successful product launches and has aggressively cut its costs and improved its margins (including new facilities in China). You can expect EPS to grow more quickly in the coming years. The company has a strong profile and not including this stock in your portfolio or watch list would be a mistake. The drop in sales of COVID-19 testing kits is still having an effect, but the Nutrition and Medical Devices segments are offsetting the headwinds, and it can count on its FreeStyle Libre blood glucose monitor franchise to support growth.

Potential Risks

No pharmaceutical company is shielded from product quality issues or recalls, and this is something that ABT could potentially face. Another possible downside is the level of competition. Although the players are not numerous in these business segments, each competitor invests heavily in R&D to develop the next innovation in its niche. ABT is slightly behind some of its competitors when we compare profitability measures. Still, they are improving in this regard as they allocate large sums of money to R&D. The company must keep performing well and showcasing its strengths to the market, particularly in the molecular diagnostics sector, as it competes with other large players like Roche, Qiagen, and Hologic.

I know how hard it is to invest when stocks don’t seem to trade at their fair value

Don’t you hate not knowing when to buy or sell stocks? There are too many investing articles contradicting one another. This creates confusion and leaves you with the impression you will not reach financial independence. It doesn’t have to be this way. I’ve built a free recession-proof portfolio workbook which will give you the actionable tools you need to invest with confidence and reach financial freedom.

This workbook is a guide to help you achieve three things:

- Invest with conviction and address directly your buy/sell questions.

- Build and manage your portfolio through difficult times.

- Enjoy your retirement.

Leave a Reply